Foreign currency (FX) deposits are among the key indicators used to evaluate the effectiveness of monetary policy and assess financial stability. The termination of the FX-protected deposit (KKM) accounts, gold price movements, and the rise in euro-US dollar exchange rate were among the factors leading to the recent increase in foreign currency deposits. In this blog post, we summarize the related recent trends in FX deposits.[1]

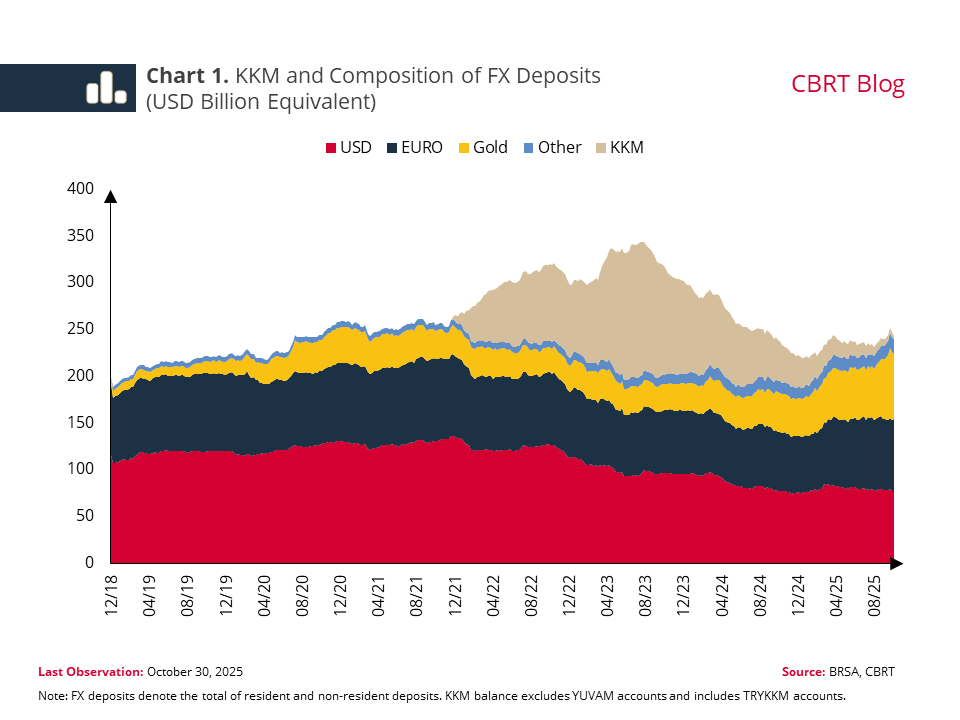

As of August 2023, KKM accounts reached their highest amount, with the sum of KKM and FX deposits exceeding USD 340 billion. In the following period, depositors' preference for Turkish lira deposits strengthened as a consequence of the tight monetary policy stance and complementary macroprudential policies. After declining to USD 221 billion at the end of 2024, the total amount of KKM and FX deposits rose again recently, reaching USD 242 billion (Chart 1).

FX deposits rose by USD 50 billion since the end of 2024, from USD 188 billion to USD 238 billion. Of this increase, gold deposits and euro deposits accounted for USD 31 billion and USD 15 billion, respectively. The remaining portion was due to USD and other FX deposits.

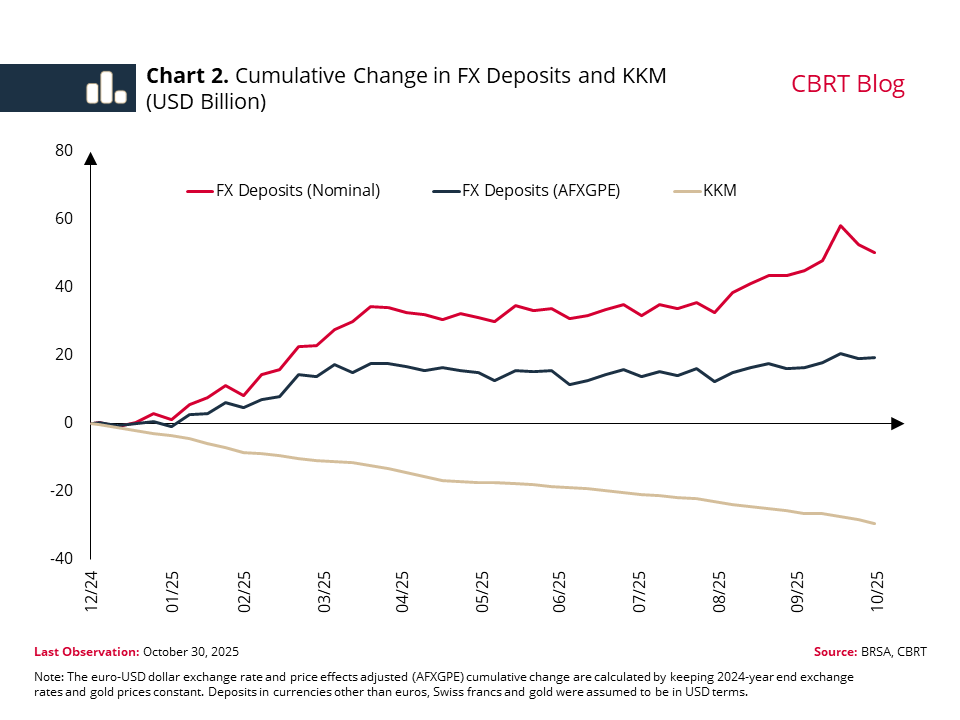

In 2025, the nominal rise in FX deposits was largely driven by the rise in the euro-US dollar exchange rate and gold prices. The price of gold per ounce, which was around USD 2,600 at the end of 2024, reached its peak value of USD 4,500 on October 17, 2025 marking an approximately 73% increase, before settling to USD 4,000 at the end of October. During the same period, the euro-US dollar exchange rate increased from 1.04 to 1.16. After adjusting for the exchange rate movements and valuation effects, the total increase of USD 50 billion in 2025 becomes USD 19 billion, with USD 6.5 billion of this amount coming from real persons’ accounts (Chart 2).

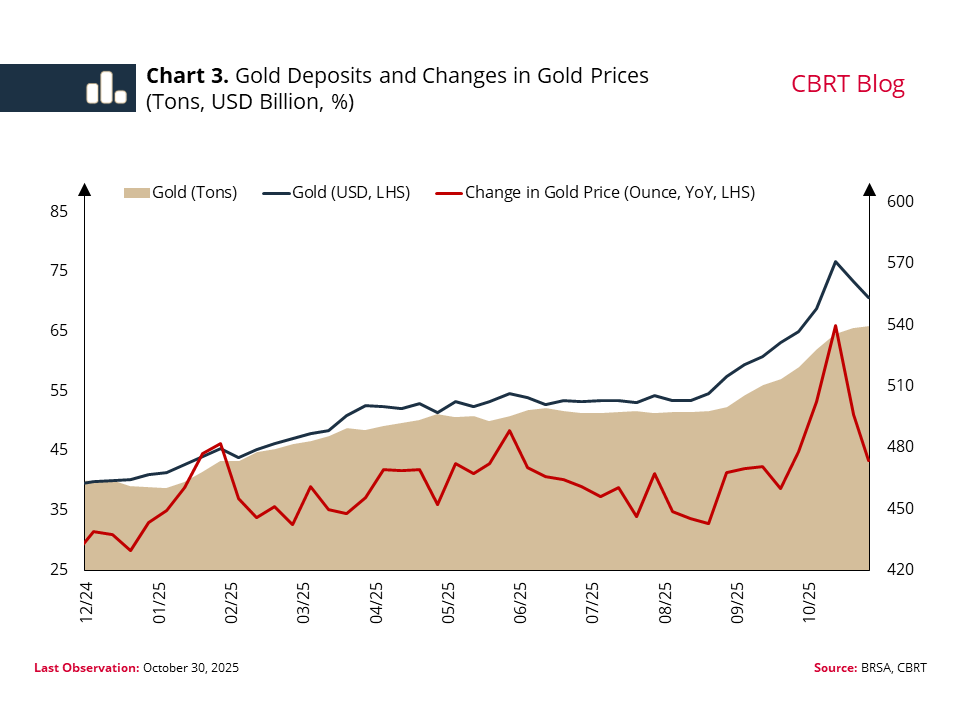

The rise in global gold prices also had an effect on portfolio choices. The fact that the returns from gold particularly in September and October were significantly above those of other financial instruments led to a stronger demand for gold deposits. Indeed, we see an increase in the tons of gold contained within the deposits. Gold deposits have increased by approximately 76 tons in 2025, corresponding to a USD 6.5 billion rise at constant prices, with more than half of this change occurring in the last two months (Chart 3).

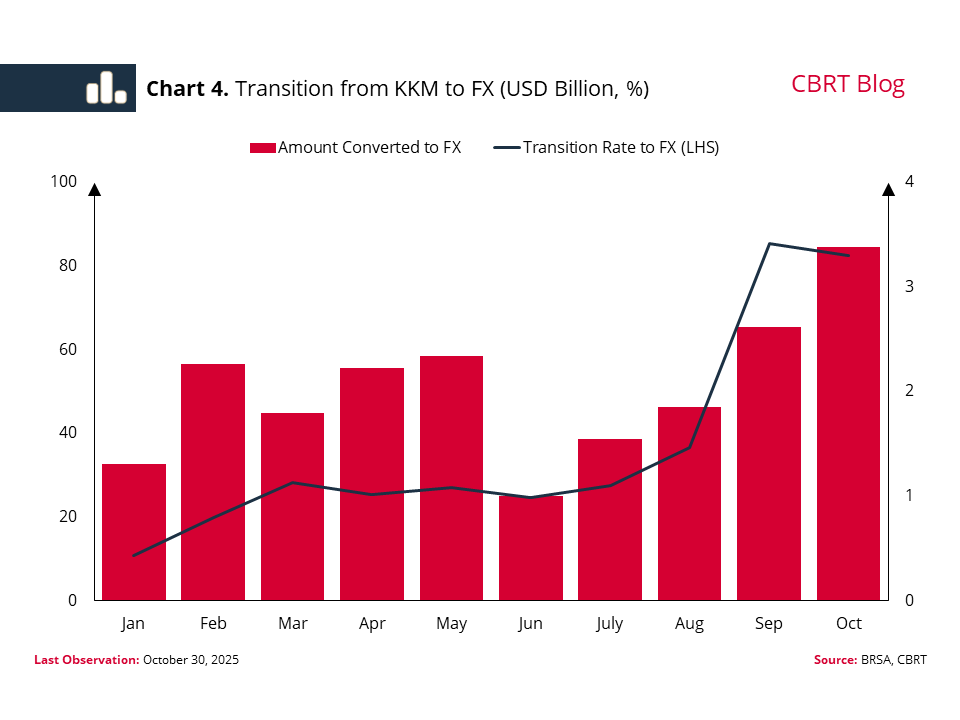

The transition from KKM accounts to FX was also among the drivers of the increase in FX deposits. In the same period, the KKM balance decreased by USD 29 billion, falling to below USD 4 billion. The conversion rate from these accounts to FX was around 25% from March to August. Following the termination of the opening and renewal of KKM accounts for real persons as well in August, this rate exceeded 80% in September and October. This rise was expected given the strong FX tendency of the remaining KKM depositors. In fact, measures such as targets for transition to TRY could be introduced to ensure that the conversion to FX remained limited during the termination of KKM accounts as in the previous periods. However, in order to safeguard financial stability and market functioning, the macroprudential framework was simplified and all targets related to maturing KKM accounts were abolished. In this respect, the conversion from KKM accounts to FX amounted to USD 7.9 billion in the August-October period (Chart 4). It is also worth noting that KKM deposits are expected to be largely wound down by the end of November.

To sum up, FX deposits have been increasing due to movements in the euro-USD dollar exchange rate and valuation effects. FX deposits adjusted for price and exchange rate effects, on the other hand, have increased less, with the termination of KKM accounts and demand for gold deposits the likely culprits for this increase. Despite the surge in gold prices, the share of TRY deposits remains at historical averages. These developments suggest that households and corporations have largely maintained their preference for TRY assets.

[1] The share of mutual funds in the financial system has recently been on the rise. However, this study aims to analyze the recent course of FX deposits and the determining dynamics.